ExxonMobil vs. Chevron: The Illusion of Revenue Scale

3 minute readPublished: Wednesday, July 1, 2026 at 3:10 pm

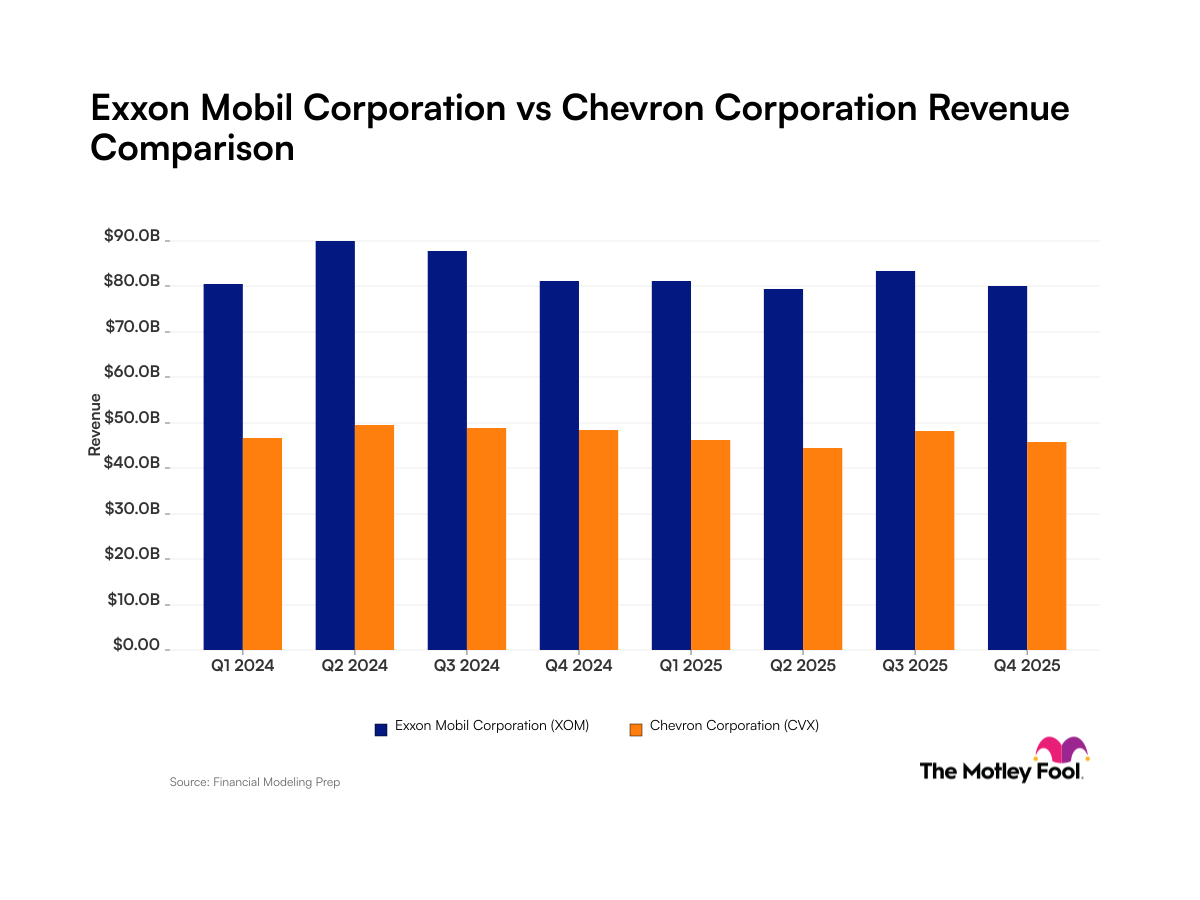

ExxonMobil and Chevron, the preeminent forces in the oil and gas industry, present a compelling case study for investors, revealing that sheer revenue scale does not always dictate profitability. While both are integrated giants and significant dividend payers, ExxonMobil consistently outpaces Chevron in terms of overall revenue.

ExxonMobil's revenue streams are diverse, encompassing the global exploration, extraction, and refining of oil and natural gas, alongside the production of commercial petrochemicals, olefins, and specialized chemical products. Recent developments include a preliminary agreement to supply liquefied natural gas to South Africa and a favorable Supreme Court ruling in Cuban litigation. For the quarter ending March 31, 2026, the company reported a net income margin of approximately 5%.

Chevron, mirroring ExxonMobil's core operations, also generates revenue through the exploration, extraction, pipeline transportation, and refining of crude oil and natural gas, as well as the production of industrial petrochemicals. The company recently entered into a power agreement with Microsoft in Texas and recorded an earnings before interest and tax, or operating margin, of 7% for the quarter ending March 31, 2026.

Revenue, defined as the gross amount a business generates from its core operations before expenses and taxes, is a fundamental metric for investors. Data as of June 23, 2026, indicates that ExxonMobil typically generates over 70% more revenue than Chevron each quarter. This top-line advantage is supported by a substantial physical asset base and significantly higher daily production volumes. ExxonMobil achieved a 40-year high in its 2025 annual production, reaching 4.7 million barrels of oil equivalent per day, with notable contributions from the Permian Basin and Guyana.

Interestingly, while ExxonMobil's total revenue significantly exceeds Chevron's, their upstream revenues are surprisingly close. This disparity is largely attributed to ExxonMobil's extensive international downstream refining operations and its higher overall daily production. Chevron also saw record production in 2025, but its net production of 3.7 million barrels of oil equivalent per day fell short of ExxonMobil's. Both companies have pursued aggressive growth strategies; ExxonMobil's $60 billion acquisition of Pioneer Natural Resources in 2024 bolstered its production, particularly in the Permian Basin. Chevron, in turn, acquired Hess for $53 billion in 2025, expanding its presence in Guyana and the Bakken.

Despite ExxonMobil's larger revenue base, a greater revenue does not automatically translate to higher profits, largely due to differences in downstream operations. Over the trailing twelve months, both companies posted operating margins of around 10%. Ultimately, both ExxonMobil and Chevron are considered titans of the energy industry and solid long-term investments for those focused on the sector.

BNN's Perspective:

The analysis highlights a crucial distinction for investors: revenue is a measure of scale, but not necessarily of efficiency or profitability. While ExxonMobil's larger revenue base is undeniable, the comparable upstream revenues and similar operating margins suggest that Chevron is effectively leveraging its assets. This underscores the importance of looking beyond headline figures to understand the underlying operational strengths and strategic decisions of these energy giants. Both companies appear to be well-positioned for the long term, offering investors different avenues for exposure to the energy market.

Tags: ExxonMobil, Chevron, revenue, oil and gas, integrated oil companies, dividend stocks, liquefied natural gas, petrochemicals, upstream, downstream, operating margin, production volumes, Permian Basin, Guyana, Bakken, Pioneer Natural Resources, Hess